The cloud’s tenuous relationship with AI

Share!

When you think about the impact of AI in recent years on the cloud companies, it’s pretty easy to make a connection between the rise of AI and increasing revenue for cloud infrastructure companies.

Just this month, we heard about Oracle making some wild cloud revenue projections in the coming years, growing from $18 billion this year to $144 billion by 2030. As I wrote earlier this week, that’s all related to AI. In particular, a single deal between Oracle and OpenAI could be worth up to $300 billion when all is said and done. That’s a lot of eggs in one basket, especially when that company is spending exorbitant amounts of money on infrastructure to support the deal.

OpenAI has also made deals with Google Cloud, CoreWeave and of course, Microsoft. The latter is a case of ongoing drama as the two companies try to figure out how they will work together moving forward.

While there is no known deal on the table with Amazon, it feels like it’s only a matter of time. OpenAI has a seemingly endless hunger for resources, and that’s the last major player it has yet to get into bed with.

Anthropic, on the other hand, prefers Amazon, which has helped finance it to the tune of $8 billion in much the same way that OpenAI and Microsoft have played together. Anthropic also runs primarily on AWS infrastructure. It’s all extremely complicated and there are too many examples to mention them all, but there is a lot of AI infrastructure money out there, so much so that it makes me wonder what will happen if the market slips a bit.

What ripple effect could that have across the technology industry and, indeed, the entire economy? It’s a subject worth exploring.

Data centers everywhere

As I wrote in February, generative AI is feeding a voracious appetite for infrastructure investing. In 2025 alone, spending forecasts included $100 billion each from Amazon and OpenAI. You can throw in another $80 billion from Microsoft, $75 billion from Google and $65 billion from Meta – $420 billion in all. Add to that the $40 billion commitment to data center construction in the U.K. announced this week — and pretty soon you’re talking real money.

In fact, some of that money is already being put to work. CapEx reached epic heights last quarter climbing to $127 billion, up 72% year over year, per Synergy Research’s latest data. Data center investment accounted for the vast majority of the money. It begs the question if this level of spending has limits, but Synergy reports “total hyperscale company revenues in Q2 totaled $720 billion.” It appears that these companies can afford it for the time being, keeping in mind all of that revenue isn’t evenly distributed, and some will struggle more than others to keep up with the building boom. As they build with such fervor, it’s fair to ask what would happen if some of that promised business failed to materialize.

There’s also the effect of this level of spending on the economy at large. Consider that investor and tech expert Paul Kedrosky wrote in a July blog post: “AI capex may be ~2% of US GDP in 2025, given a standard multiplier. This would imply an AI contribution to GDP growth of 0.7% in 2025.”

And there are big questions about power and water consumption, and the impact these data centers could have on the environment and the broader economy as AI drains a variety of resources. These concerns, in turn, raise the prospect of more stringent regulation from local, state or federal governments. Put all of this together, and it’s not just the cloud vendors who face the risk of this building boom slowing down. If AI investment dries up, what will the overall fallout be?

Risky business

This level of spending can be a double-edged sword. On one hand, it’s driving enormous investment, pushing up revenue projections, and also generating tremendous revenue right now for cloud infrastructure vendors and downstream vendors alike.

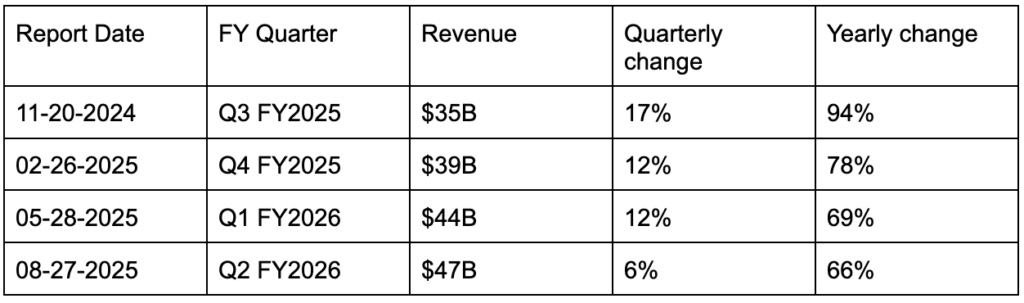

Look at Nvidia as a prime example of this. The company’s GPUs are in high demand, driving up prices and creating enormous value. Have a look at the revenue over the last four quarters:

While the rate of growth is predictably dropping over time, the revenue continues to increase at a rapid rate and Nvidia stock continues to perform well, up 54% over the last year and 26% for the year to date.

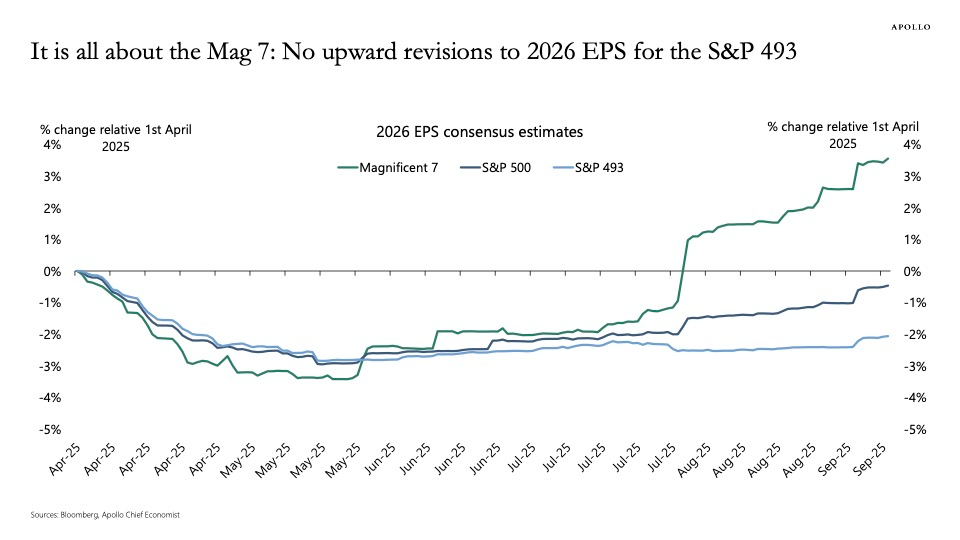

But it’s not all necessarily positive. As Apollo chief economist Torsten Sløk noted in his newsletter this week, the AI boom is fueling heavy stock market investment with much of that money concentrated in just a few tech names tied to AI. “The bottom line is once again that there is an extreme degree of concentration in the S&P 500, and equity investors are dramatically overexposed to AI.” He included this chart to illustrate his point:

This is all to say that AI is attracting incredible levels of capital and spending. AI advocates would argue that it’s working as designed. This is a tremendous opportunity, akin to the build out of the internet in the late 1990s, and the level of money being spent is entirely appropriate.

But such a level of spending carries with it uncertainty too. As Jerry Neumann wrote in the Colossus article "AI will not make you rich," there is a real risk that some investors could come up empty.

It’s well worth reading the whole piece, but as he sees it, there isn’t any true "innovation phase" happening here. Instead of thousands of entrepreneurs building lots of new things with no clear leaders, as in the early days of the personal computer, there are instead just a handful of models. It took a number of years for the PC winners to shake out. With AI, the power is already concentrated where you would expect with incumbents like Google and Microsoft, and large new players like Anthropic and OpenAI.

“But because [builders] are using models owned by the big AI companies, their ability to fully experiment is limited to what’s allowed by the incumbents, who have no desire to permit an extended challenge to the status quo,” Neumann wrote.

All of this brings us back to the cloud infrastructure vendors where we started. There is a tremendous amount of capital flowing with gobs of money to be made from the current AI boom. There is also much more projected down the road, but there is a real danger that investors get spooked, or a large buyer like OpenAI can’t keep raising the money required for these continued investments, and the money spigot slows to a trickle. And it makes me wonder what impact it will have across the industry and the economy should that happen.

~Ron

Featured image by Igor Omilaev on Unsplash