Microsoft, Google chip away at Amazon’s cloud dominance as neoclouds rise

Share!

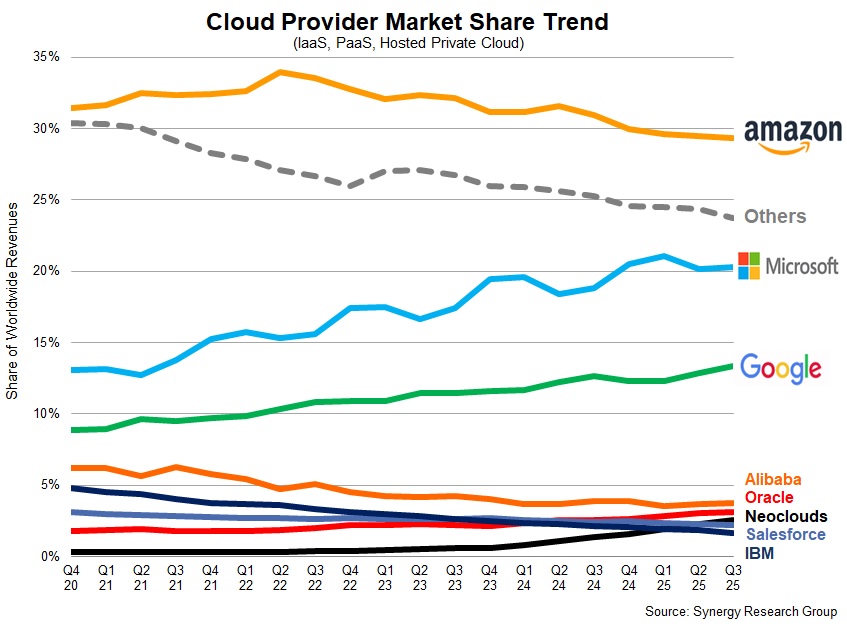

We reported on the cloud infrastructure numbers recently, and there was a lot of good news. For the first time, it reached $100 billion for a quarter, and we saw the largest players still growing at fairly substantial rates, especially for their size. Synergy Research reports that the big three now control 63% of worldwide market share, a number that continues to creep up, putting pressure on the players at the lower end of the market, no matter how large their growth numbers may be.

“The huge gulf in scale between the big three and the rest means that no matter how fast the up-and-coming cloud providers grow, in the short term they cannot impact the market shares of the big three. They are fighting the law of large numbers, and that is a tough battle to win,” Synergy’s John Dinsdale wrote in an email.

But there is also more to the story than industry size and the share of each of the top companies. We are starting to see some subtle shifts across the cloud landscape. Just because the big three can be secure in their dominance doesn’t mean they aren’t feeling the heat from one another — or that the players at the back of the pack aren’t pushing as hard as they can..

That includes a dent in the armor of long-time market leader Amazon and the rise of the neoclouds. But against this positive backdrop, we are also seeing an enormous amount of CapEx spending, which could offset some of that growth over time.

Amazon market share nudges down

Amazon has started to see its long-time first-mover advantage erode along with its market share. It’s not substantial because as companies get larger, their relative position tends to stabilize, but it is significant enough to notice.

Consider that Amazon dropped below 30% to 29% for the first time I can remember, and I’ve been following this sector for at least 8 years. For a long time, Amazon held onto about a third of total cloud infrastructure spending, no matter how large the market grew, but as we’ve seen the rise of generative AI in recent years, it seems to have benefited rivals Microsoft and Google more (even though it’s costing these companies big bucks to build the data centers to meet the new demand).

“In truth, not a big shift from the previous quarter. Significant? Somewhat,” Dinsdale told FastForward. “Its market share over the last four quarters combined was 30%, and for the preceding four quarters was 31%. So its market share has nudged down as Microsoft and Google grow more rapidly.”

And while Microsoft and Google continue to trend upward when it comes to market share, Amazon’s share has been on a downward trend even as revenue continues to grow, as the chart below illustrates.

Here come the neoclouds

Another storyline in this quarter’s report was the rise of the neoclouds, a new generation of vendors helping companies access GPUs in a cloud model, companies like CoreWeave, Crusoe and Lambda.

In an October report, Synergy found “neocloud revenues passed the $5 billion mark in Q2, having grown by 205% from last year. They are on track to exceed $23 billion in revenues for the full year. Synergy forecasts that they will reach almost $180 billion in 2030, growing by an average 69% per year.”

While CoreWeave, a company that went public in March, is the clear leader here, the other companies are still growing rapidly.

If you’re wondering about Oracle, a company that’s received a lot of press, it still sits in the low single digits with just 3% market share in spite of its well-publicized deals with OpenAI. As Dinsdale told me recently, future revenue doesn’t add up to what’s happening in the present. And as of now, this is what the numbers show.

“Oracle are masters of making a big noise. They have signed some huge deals but these are bookings and future commitments or plans, not current revenues. Any company can shout about the future, but it is current revenue where the rubber meets the road,” he said.

One other thing to keep in mind here is the staggering cost of this revenue. As I wrote earlier this month in If you build it, will they come, CapEx exceeded cloud revenue by a fair amount at the Big Three in the most recent quarter — and a fair percentage of that spending went to building new data centers, according to the companies.

| Company | Quarterly Revenue | Quarterly CapEx spending |

| Amazon | $31 billion | $34 billion |

| Microsoft | $21 billion | $35 billion |

| $14 billion | $24 billion |

“But that AI-fueled growth potentially comes at an incredible cost: these same companies are pouring such massive sums into infrastructure that capital expenditures appear to be climbing to levels that are exceeding their quarterly cloud revenue,” I wrote in my commentary. Is that a sustainable approach?

The latest numbers show how long it takes to really impact a market in a substantial way, especially one with such dominant players. While Oracle and the neoclouds are making hay, it’s not enough to substantially move the market share needle. Perhaps the biggest thing to watch in the coming quarters is whether cloud revenue will support the current CapEx spending binge from the Big Three.

Featured image by Getty Images on Unsplash+.